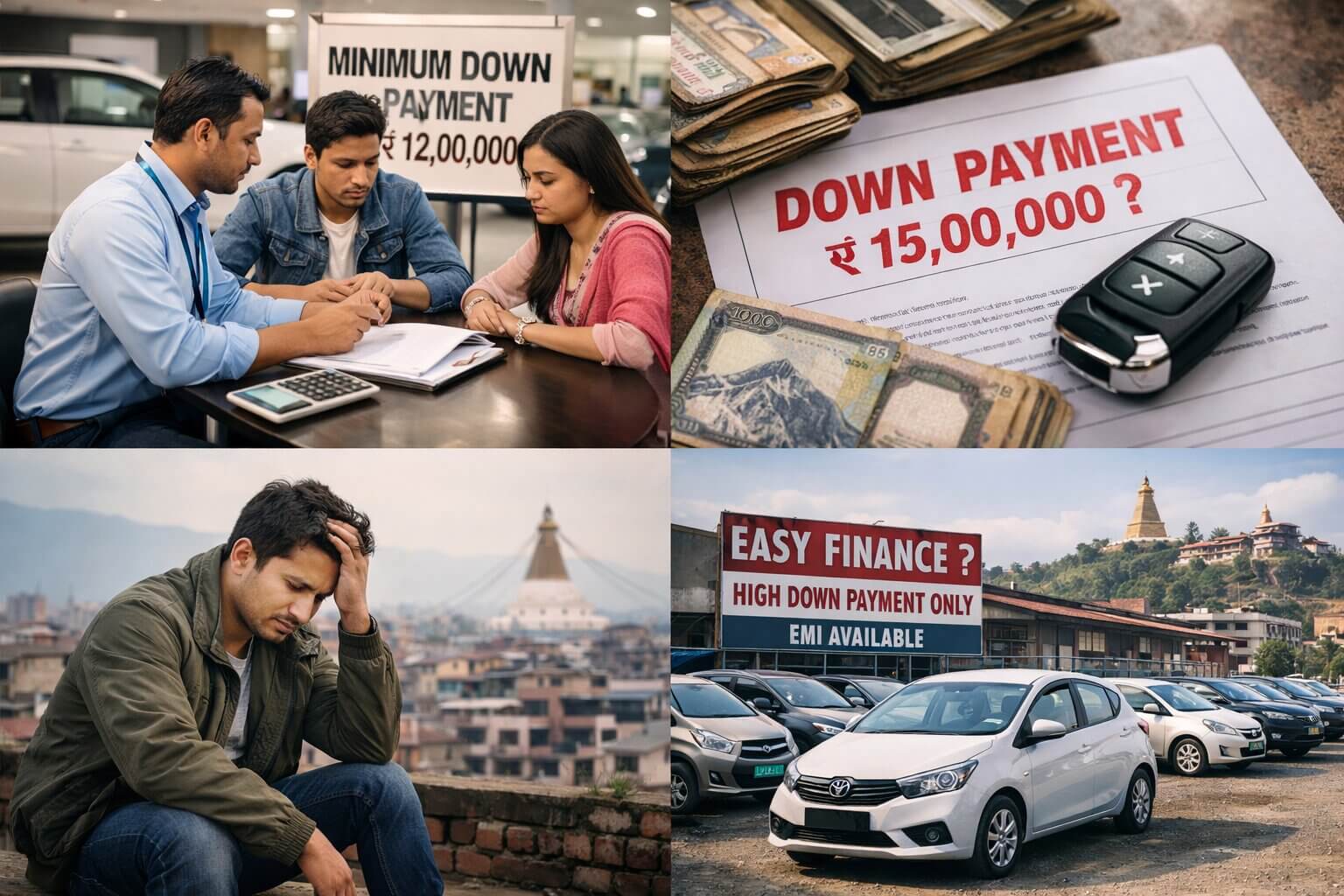

For many people, buying a car is not about luxury; it is about daily survival. Office commutes, family responsibilities, safety, and time all depend on reliable transport. Yet, when a buyer walks into a showroom or a reconditioned car house, the first assumption is often completely unrealistic. Down payment expectations of ₹8 lakhs, ₹10 lakhs, or even ₹15 lakhs have somehow become “normal,” exposing how disconnected the system is from the financial reality of the average working individual.

Table of Contents

A System Built Around Cash, Not Real People

Most showrooms operate on a simple belief: higher down payments mean safer customers. From a business and banking perspective, this reduces risk. But this logic ignores a basic truth. People who can arrange ₹10–15 lakhs in cash usually do not depend on financing at all. They either buy outright or explore better options. Meanwhile, genuine buyers with stable income and strong repayment ability are filtered out before the discussion even begins.

Suggested Read: Why Did Israel & the USA Launch a Joint Attack on Iran?

EMI Capacity Is Not the Same as Cash in Hand

There is a huge difference between owning a large lump sum and managing monthly payments. Many salaried professionals and self-employed workers may not have ₹8–15 lakhs saved, but they can comfortably pay a fixed EMI every month without fail. Rent, family responsibilities, education costs, and inflation consume savings, not irresponsibility. Still, the system continues to treat a lack of cash as a lack of capability.

Why This Thinking Is Hurting the Auto Industry?

By insisting on massive down payments, showrooms and reconditioned car houses are pushing away genuine customers. Flexible financing with lower upfront payments would immediately open the market to a much larger audience. In reality, a customer who pays EMIs consistently for four or five years creates more long-term value than a one-time cash buyer. High entry barriers don’t protect the market—they shrink it.

Why Dealers and Banks Refuse to Adapt?

The current model exists primarily to protect institutions, not customers. Banks want to avoid defaults, dealers want to avoid recovery hassles, and outdated credit evaluation systems continue to dominate. Instead of properly assessing income stability, employment consistency, and repayment history, the system still focuses on how much money a person can show upfront.

The Need for Smarter and Fairer Financing

Modern vehicle financing must be built around cash flow, not cash reserves. Lower average down payments, smarter EMI eligibility checks, and flexible used-car loan structures would support first-time buyers and working-class families. These changes would not increase risk they would simply spread opportunity more fairly and realistically.

The Buyer Is Not the Problem

The real issue is not that people cannot afford cars. The issue is that the system refuses to acknowledge how people actually earn and spend today. Buyers are willing to pay, capable of paying, and serious about ownership. What they lack is a system that understands real life instead of clinging to outdated assumptions.

Latest Posts

Nepal’s National Assembly Passes Landmark Tourism Bill with Toughest-Ever Everest Rules

Zero Down Payment” Bike Promotion Turns Out to Be Misleading, Customers Speak Out

China’s BYD Becomes World’s Top Electric Vehicle Seller, Overtaking Tesla